📝 usncan Note: The AI Revolution in HR And How VC is Reshaping The Future Of HR Tech

Disclaimer: This content has been prepared based on currently trending topics to increase your awareness.

The HR tech sector stands at an inflection point. As artificial intelligence transforms how organizations manage their most valuable asset, their people, venture capital continues to flood into the space. Global VC investments in the broader HR sector (“work tech” which include human capital management, talent acquisition, payroll, workforce management) were $5.65bn in 2024 growing 16% year over year, signaling a fundamental shift in how investors view the intersection of AI and workforce management. However, this growth comes after a significant correction period, as venture funding in HR technology had previously fallen to a three-year low following years of heightened investor interest.

This transformation extends far beyond simple automation. Today’s AI-powered HR tools are reshaping everything from recruitment and employee engagement to performance management and retention strategies. Two years ago, Goldman Sachs analysts reported that AI-powered technology investment “could approach $100 billion in the U.S. and $200 billion globally by 2025”, with HR technology representing a significant portion of this investment surge and this forecast is on track.

At the same time, it is important to recognize that AI adoption in HR remains uneven. Many organizations are still at the experimental stage, piloting tools in recruitment or engagement surveys but not yet embedding them deeply into core HR processes. Surveys from Gartner and Deloitte show that while intent to adopt AI in HR is high, actual implementation often lags due to integration challenges, cultural resistance, and concerns about fairness and transparency.

The Expanding Market Opportunity

The numbers tell a compelling story of exponential growth. Fortune Business Insights, states that the broader HR tech market was estimated at $37.66 billion dollars in 2023 and is expected to reach $81.84 billion dollars in 2032, demonstrating the broader transformation occurring across all HR functions, not just employee engagement. Also per Fortune Business Insights, as a segment of broader HR tech market, global employee engagement software market size is projected to grow from $1.22 billion dollars in 2025 to $3.52 billion dollars by 2032, exhibiting a CAGR of 16.3%. However, various market research firms present slightly different projections, with Grand View Research stating that global employee engagement software market size is estimated at $928.3 million in 2023 and anticipated to grow at a CAGR of 16.4% from 2024 to 2030. The lack of standardized market definitions makes it difficult to assess the true addressable market for AI-specific HR solutions.

This definitional challenge is more than academic—it has real implications for investors and operators. Overstating the total addressable market (TAM) can lead to inflated valuations and misaligned growth strategies. HR departments often operate under tight budgetary scrutiny, meaning that willingness to pay may not scale as easily as market forecasts suggest. For startups, this makes demonstrating clear ROI a prerequisite for meaningful adoption.

The HR tech market growth is being driven by several converging factors. The post-pandemic workforce has fundamentally changed expectations around work-life balance, career development, and employee experience. Meanwhile, the war for talent has intensified across industries, making employee retention a critical business imperative. Organizations are discovering that traditional HR approaches, often reactive and based on annual surveys, are insufficient for managing today’s dynamic workforce.

Venture Capital’s Strategic Bet on HR AI

The venture capital community has taken notice. Within this broader AI investment boom, HR technology has emerged as a particularly attractive sector.

Recent high-profile funding rounds illustrate this trend. Mercor, the AI recruiting startup founded by three 21-year-old Thiel Fellows, has raised $100 million in a Series B round, achieving a $2 billion valuation. This represents the kind of aggressive valuation multiples investors are willing to pay for AI-first HR platforms that demonstrate strong product-market fit.

The investment thesis is straightforward: HR represents one of the largest cost centers in most organizations, yet it has been slow to adopt advanced technology. The opportunity to create significant efficiency gains through AI automation, while simultaneously improving employee outcomes, presents a compelling value proposition for both startups and their investors.

Tier 1 VC funds which have a successful track record in HR tech sector include Index Ventures, Accel, Bessemer, Insight Partners and General Catalyst.

Yet, this investor enthusiasm carries its own risks. As seen in prior HR tech waves (e.g., the boom and bust of early-2010s recruitment marketplaces), capital can outpace actual enterprise demand. Startups may scale prematurely, burning cash on customer acquisition before proving retention or long-term value. There is also a danger of “AI washing”: companies marketing superficial AI features to attract investment rather than building genuinely differentiated technology. For VCs, the challenge lies in separating enduring innovation from hype.

The unit economics challenge is particularly acute in HR tech: according to SaaS Capital’s 2025 spending benchmarks survey of over 1,000 private B2B SaaS companies, the median company spends 13% of ARR (annual recurring revenue) on sales and 8% on marketing, with only 46% of equity-backed SaaS companies achieving profitability. Companies that cannot demonstrate clear path to positive unit economics within reasonable timeframes face increasing scrutiny from investors.

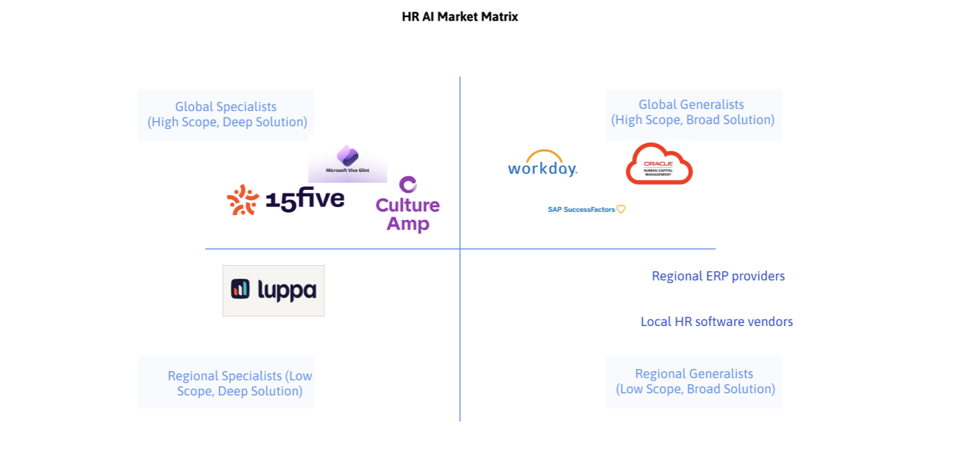

Market Dynamics: Global Giants Vs Specialized and Regional Providers

To understand the competitive landscape, it’s useful to examine the HR AI market through a strategic framework that considers two key dimensions: market scope (global vs. regional focus) and solution depth (broad platform vs. specialized functionality).

HR AI Market Matrix

Josipa Majic Predin

Global Specialists (High Scope, Deep Solution)

- Players: Culture Amp, 15Five, Glint (now Microsoft Viva Insights)

- Characteristics: Best-in-breed functionality, strong product focus, global distribution

- Strengths: Deep domain expertise, rapid innovation, strong user experience

- Weaknesses: Integration challenges, limited market penetration in emerging regions

Global Generalists (High Scope, Broad Solution)

- Players: Workday, Oracle HCM, SAP SuccessFactors

- Characteristics: Massive scale, comprehensive HR suites, significant R&D budgets

- Strengths: Brand recognition, extensive integration capabilities, enterprise sales expertise

- Weaknesses: Slow innovation cycles, one-size-fits-all approach, limited localization

Regional Generalists (Low Scope, Broad Solution)

- Players: Regional ERP providers, local HR software vendors

- Characteristics: Geographic focus, broad but shallow functionality

- Strengths: Local market knowledge, regulatory compliance, established partnerships

- Weaknesses: Limited innovation resources, technology debt, scalability constraints

Regional Specialists (Low Scope, Deep Solution)

- Players: specialized solutions such as Luppa and other AI regional employee engagement platforms, niche HR tools

- Characteristics: Deep regional focus, specialized functionality, cultural adaptation

- Strengths: Localized insights, agile development, market-specific features

- Weaknesses: Limited scale, resource constraints, narrow market reach

The tension between global platforms and regional specialists is unlikely to resolve quickly. On one hand, global providers offer reliability, compliance, and integration at scale. On the other, regional players can embed cultural nuance and local regulation more effectively. The open question is whether enterprises will ultimately prioritize global consistency over localized relevance—or whether a hybrid ecosystem will emerge where global platforms acquire or partner with regional innovators.

The Dark Horse: Specialized, Regional Providers With A Contrarian Strategy and Capital Efficiency

In this competitive landscape, nimble companies like Luppa represents an intriguing contrarian bet. While most venture-backed HR AI companies are pursuing global scale from day one, Luppa has deliberately chosen to go deep rather than wide, focusing specifically on Southeast and Eastern Europe.

This strategy challenges conventional Silicon Valley wisdom about market sizing and scalability. Instead of competing directly with well-funded global players, such smaller players are remailing capitally efficient and are building competitive moats that are difficult for larger companies to replicate: market-specific benchmarks, localized algorithms, culturally adapted experiences, local integrations, and strong regional partner networks.

Such approach has the potential to adress a fundamental weakness in many AI-powered HR tools: cultural and regulatory context matters enormously in human resources. What works in Silicon Valley may not translate effectively to Sofia, Belgrade, Budapest, or Bucharest. By focusing on these markets, specialized regional providers can develop deep expertise that global competitors would struggle to match without significant local investment and teams on the ground. However, we have seen European, Indian and Israeli HR tech platforms scaling globally after launching locally.

From a market sizing perspective, Luppa’s thesis is that even a focused regional strategy can generate substantial returns. The company estimates that capturing just 10% market share in Southeast and Eastern Europe could generate €60 million in annual revenue, a meaningful scale for any company – reglardless of funding and strategy.

Still, regional specialists face an uphill battle. While capital efficiency and localized differentiation are attractive, many such startups struggle when attempting to cross the chasm from regional success to pan-European or global scale. European history is full of promising HR startups that plateaued at €10–20 million ARR (annual reccuring revenue) because of fragmented regulations, heterogeneous languages, and sales execution challenges. Startups like Luppa are betting bold, but not without risk.

The AI Differentiation

What sets companies like Luppa apart isn’t just its geographic focus, but its approach to artificial intelligence. While many HR platforms have retrofitted AI capabilities onto existing systems, Luppa has built AI-first architecture from the ground up. The company’s proprietary AI system analyzes company data, market benchmarks, and industry best practices to generate concrete, tailored recommendations.

Luppa AI pulse survey

Luppa AI

Perhaps most intriguingly, the company claims that in testing, 80% of customers couldn’t distinguish between advice generated by their AI system and recommendations from human HR professionals. If validated at scale, this suggests that Luppa may have achieved a significant breakthrough in AI-human parity for HR advisory functions.

However, AI solutions still need guardrails and must be monitored carefully. HR decisions directly affect livelihoods, promotions, and pay equity. Any AI-driven advisory system must not only deliver accuracy but also demonstrate fairness, explainability, and compliance with evolving regulations like the EU AI Act. Without these safeguards, organizations risk legal liability and reputational damage even if the underlying technology performs well.

The Road Ahead

The convergence of AI advancement and massive venture capital investment is creating unprecedented opportunities in HR technology. Global venture funding ticked up year over year in Q2 2025, reaching $91 billion dollars, with a greater concentration of capital into the largest funding rounds, suggesting that the funding environment remains robust for promising AI startups.

For companies like Luppa, the challenge will be executing on their strategic vision while the window of opportunity remains open. The regional focus strategy is compelling in theory, but will require exceptional execution to build the kind of dominant market position that justifies venture-scale returns. With this exceptional execution, at some point, there will be an ambition and push to expand across entire Europe and globally. For this expansion, it is imperative to approach with human centric design, master sustainable unit economics, and have a robust approach to regulatory compliance and data privacy.

More broadly, the HR AI revolution is still in its early stages. While the technology promises are significant—better employee experiences, reduced turnover, more effective talent management—the real-world implementation challenges are substantial. Success will require not just technological sophistication, but deep understanding of human psychology, organizational behavior, and cultural nuance. Daniel Ackerman, Founder of Luppa believes that the company is well positioned: “We are entering a golden age of HR and HR innovation. The HR AI revolution is not about replacing people, but about empowering organizations with tools that help them truly understand, engage, motivate, and retain their workforce. The future will be defined by companies that combine technical excellence with human insight – those are the ones shaping the workplace of tomorrow.”

The companies that can master this combination of technical excellence and human insight will likely define the future of work itself. Whether that future is dominated by global platforms or enriched by specialized regional players like remains to be seen. What’s certain is that the next few years will be critical in determining which strategic approaches prove most viable in this rapidly evolving market.